Step 1. Please enter the following info to obtain an accurate quote for Auto Insurance. Get multiple auto insurance quotes online now from top companies. Compare, Buy and Save!

Florida drivers face unique challenges compared to residents of other states. Between the seasonal residents, vacationers, overcrowded roads, and young drivers drivers need to navigate not only the roads but also the choice car insurance with as much care and information as possible. We’ve taken the guess work out of car insurance with this handy guide to car insurance in the sunshine state.

Some things in life we have no control over. But some things we can control.

There is a lot at stake when you get into your car: you financial, emotional and physical future may all be impacted when you are in an accident.

Being inadequately insured can be very expensive should something go wrong. It pays to take your time to gather the facts.

We’ve put together the smart guide to Car Insurance in Florida. It will answer all your questions, provide in-depth information and help you think through all of your options.

To be a legal driver in Florida, you must carry a minimum amount of car insurance. This coverage is:

1. $10,000 per accident of no-fault personal injury protection (PIP) insurance that pays

2. $10,000 of property damage liability (PDL) insurance

*If you are retired and not earning an income, you can opt-out of the lost income portion of the PIP insurance.

Your family can be included in the PIP insurance for an additional cost, but if they have their own auto insurance they are automatically excluded from your coverage.

It is important to note that if you have caused a serious accident in the past or were convicted of driving under the influence of drugs or alcohol, you may be required to carry additional policies and/or higher coverage limits.

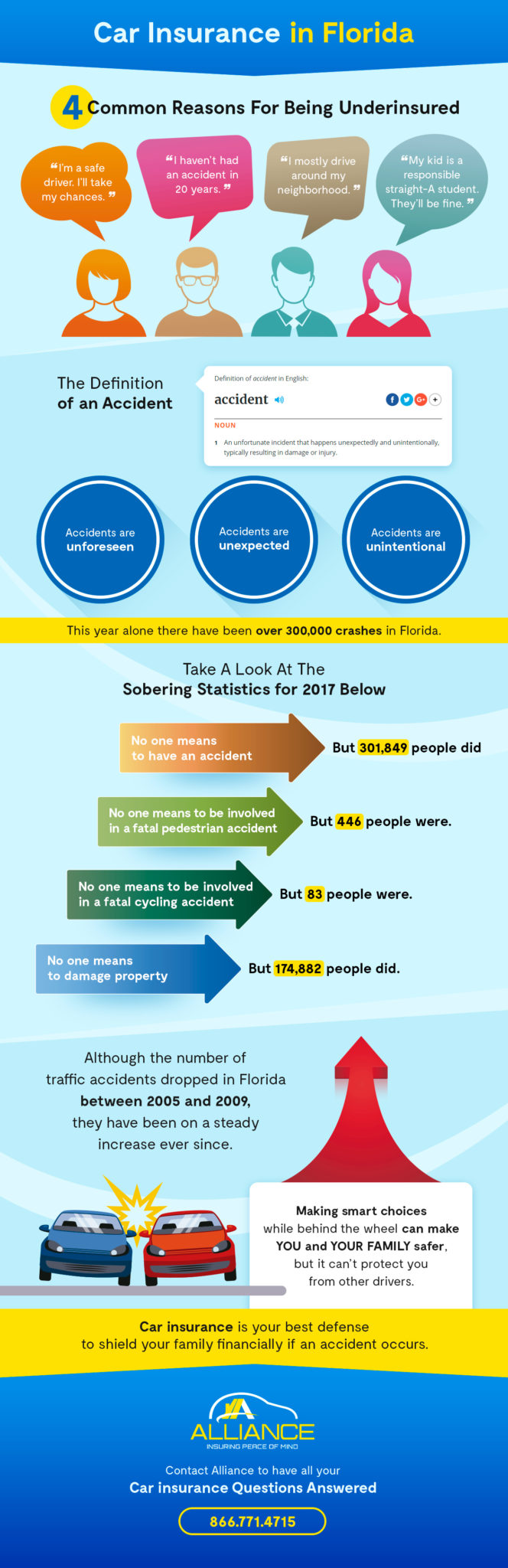

A legal driver in Florida, must carry this minimum amount of car insurance. Despite this law, approximately 24% of all Florida drivers are uninsured .

If you are in an accident and the other driver is uninsured, they may pay a fine and have their licensed suspended, but you are now solely responsible for the cost of repairing your vehicle.

Florida is a “no fault” insurance state, which means that the insurance you purchase covers the cost of your medical expenses from the accident, regardless of who caused it. However, the driver who is found to be at fault in the accident is required to pay for the property damage the other driver experienced, so it is actually a mix of no-fault and at-fault requirements. Still, whether it is a simple fender-bender in a parking lot or a crash at an intersection, how well you and your family are protected is determined almost solely by the amount of coverage you carry.

Under the no-fault rules, you must exhaust your PIP limits before suing the other driver for medical and other economic losses you’ve incurred. Even then, you cannot sue for pain and suffering, or other non-economic losses.

There are four exceptions to the no-fault system, which allows you to pursue a claim against the at-fault driver, including pain and suffering, which are:

Under Florida’s no-fault rules, you should carry the amount of insurance you need to protect yourself from high medical bills as well as the physical damage done to the other driver’s vehicle if you are found to be at fault. For many people, this means purchasing coverage beyond the minimum requirements.

Florida drivers can purchase many types and levels of additional coverage, depending on their needs, risk comfort levels, budgets, and financial reserves. There are several insurance policies that are highly recommended for Florida drivers, and others that are available if desired. Recommended coverages include:

This coverage pays for the other party’s medical expenses from injuries they suffered from an accident you caused. Although the PIP coverage will pay for their medical bills, their insurance company may come after you for these costs. This coverage is also important if the injured person was a pedestrian with no insurance or if the person’s injuries were so severe as to be an exception to the no-fault rules. In these situations, you are responsible for paying these expenses unless you have BIL insurance.

Given the high percentage of uninsured drivers in Florida, this coverage is a smart choice. It will pay your bodily injury costs if you are hit by an uninsured motorist as well as loss of income. Most insurance companies require that you purchase BIL coverage before you can purchase the uninsured motorist protection, and both are well worth the cost.

This coverage protects you from paying out of pocket costs to repair or replace your vehicle if the damage is over $10,000, the driver is uninsured, or you caused the accident. It can save you a lot of money, especially if any of the cars in the accident were totaled.

The required PIP caps your benefits at $10,000 per accident, but you still have deductibles. This policy will pay the 20% of your medical expenses and an extra 25% of the loss of income benefits, as long as the total cost of the personal injury protection benefits remains within the $10,000 limit.

Some insurance policies can protect your assets or simply make life easier in the event of an accident. These are:

This coverage also addresses medical expenses for treatments such as surgeries or dental care that is required to address your injuries. It has a separate limit from the PIP, and automatically covers any relatives that live with you. Some people find this level of coverage redundant since they have health insurance, so it is a good idea to evaluate your needs before you decide.

If the accident makes your car un-drivable, this coverage pays for the cost of getting the car from the site of the collision to the nearest insurance-authorized auto repair shop for evaluation and service.

Whether your car is working or not, you need to get to work, school, the grocery store, etc., and without this coverage, you will be paying the rental fees yourself. You need to decide if the extra cost is worth the value you will receive.

Florida minimum coverage requirements are just that – the minimum. It doesn’t afford you the protection you need against uninsured motorists and often doesn’t cover the full cost of an accident. Purchase the level of insurance that truly addresses your known risks and protects your assets.

Car insurance is expensive, but necessary, and you do get what you pay for. That doesn’t mean you have to pay top dollar for a great policy. Follow these tips to reduce your rates:

You need car insurance, but you can be smart about how much you pay. When comparing companies, ask about available discounts. You might be surprised by how much you can save.

Your teenager may be ready to drive, but it’s going to cost you. On average, adding a teen to a car insurance policy can nearly double your costs, but it can be as much as $2,000 less expensive than getting them their own policy. The reason for this higher cost is simple: they are the riskiest drivers on the road. Although teens make up only 6% of the driving population of Florida, they are involved in 14% of the fatal crashes, which is the number one cause of death for teens between the ages of 16 and 19.

Before you hide the car keys, remember that several discounts may be available to reduce the cost of car insurance for your teen, depending on the company you choose. These can include:

Students who delay getting their license are also less expensive to insure, since rates drop each year until they are 20. Also, don’t purchase the expensive, flashy car for your teen to drive since this alone will raise your rates, and having a teen driver behind that wheel will raise it even more.

Many people struggle to find the best policy for the lowest price that meets their needs. The following steps will help you select the right policy for you:

This can be a time consuming process, but it is worth it to save you money and hassle down the road. Remember, the policy you select will protect you, your family, and your assets, so it is worth making the effort to get it right.

At Alliance, we take the hassle out of purchasing car insurance. We are a BBB A+ rated company that represents the best car, home, and health insurance companies in Florida, including Travelers, Progressive, Florida Blue and more. Tell us your budget and your needs, and we will find you the best policy that meets your requirements. Let us do the research, and you will receive a selection of policies for a side-by-side comparison. Have questions? Just call (866)771-4715 to speak with one of our experienced agents.

1. Visit an Insurance Company or Check The Company Website

Whether you are busy or not, it really pays to have a slice of your time to spend in search for an auto insurance Florida. Shopping for an insurance company is like shopping for your clothes or household items – you only want what’s the best. If you prefer online shopping, no worries. Visit an auto insurance comparison website and fill out the forms there. In no time, you will have a list of top rated auto insurance companies to choose from.

2. Keep the Insurance Cost at its Lowest

After comparing multiple auto insurance companies in Florida, keep the costs down by sticking on these tips:

Getting a car insurance can be costly but you can trim the cost of keeping it with the steps that we have for you. Following these tips will not only save you money but will also get your vehicle insured for accidents.

In Florida, car insurance needs are: $10,000 for the personal injury protection, as well known as the PIP, or $10,000 for the property damage liability as well known as the PDL. And Floridians aren’t alone while it comes about having the state imposed auto insurance requirements. All the states in America need the minimum car insurance need. Whereas some of the people select to satisfy the car insurance needs by buying the policy through the insurance company, and other people select to get “self-insured,” and to put down the bond that can cover amount of car insurance needs. How you select to show proof, which you have met the state’s car insurance needs are up to state.

At times drivers are needed to buy the bodily injury protection; the cases generally fall in hands of the drivers that have been in the accident and drivers who are convicted of the offense like driving under influence driving while intoxicated. Prior to you start the search for the policy that meets the Florida’s insurance requirements, ensure that you are qualified to have this minimum coverage – and not all the drivers are. In case, you have borrowed some money to buy the new car, then your lender may undoubtedly need you to buy more than the minimum needs until debt is paid. In order, to get quotes free & learn about the insurance visit recommended sites.

Google

Tips On How To Get Cheap car insurance quotes Florida Rates

Right now, you may feel overwhelmed with all of the available car insurance information to sift through. The task may be daunting to you, or you may not be sure where you can obtain the best information about auto insurance. Fortunately, you will find below, the best auto insurance tips available.

When purchasing car insurance for your teen, remember that there are a number of ways you can get a discount. If your teen: has taken Driver’s Ed, maintains good grades, drives a car that is older, a four-door sedan or a station wagon, and/or any color but red, you could save a lot of money!

To save money on your car insurance shop for it before shopping for a new vehicle. Besides your driving record and location, the biggest factor in your price is the car they are insuring. Different companies will set different rates that are also based on their experiences paying claims for that type of car.

People looking to save money on auto insurance should remember that the fewer miles they drive, the more insurance agents like it, because your risk goes down. So if you work from home, make sure to let your agent know. There is a good chance you will see the impact on your rate in the next billing cycle.

To save money on auto insurance, be sure to take your children off of your policy once they’ve moved out on their own. If they are still at college, you may be able to get a discount through a distant student credit. These can apply when your child is attending school a certain distance from home.

There are a number of added protections available to you that are that are beyond the legally required minimum. Your premium will be higher with these options, but some are worth the added expense. Uninsured motorist coverage will protect you in the event that you are in an accident that involves either a hit-and-run or someone who is not carrying insurance.

If available in your state, request a copy of your driving history before shopping for car insurance. Information can be inaccurate on it which may be causing your quotes to be higher. Make sure you know what is on your report and if you find discrepancies have them corrected as soon as possible.

You can now feel more knowledgeable, and confident, about your understanding of auto insurance. Feel free to access all information available to you. The more you know, the better your experience will be with regard to auto insurance. You will have the most success when you keep these tips in mind.

“I am happy in today’s world to be able to compliment someone, not everyone enjoys doing what they do as Lisa did. I am on disability, was in the insurance field years ago in the 70’s and then went into the medical field and finished as a clinical supervisor. I know what I expected of my staff and Lisa exceeded all expectations. We just found your site the other night but I can assure you as our needs come up for different things we WILL be calling ALLIANCE.”

D. Clair – Florida“Felicia was a wonderful agent and helpful at every time. I would highly recommend getting your insurance needs met here.”

S. Miller – Jacksonville, FLYou were willing to take this bull by the horns and run with it when no one else was interested. You have no idea how HAPPY I am right now. I have been fighting this battle for over a month and you came through. You diffidently will be my first contact for any future insurance needs and I WILL refer my friends to you.”

Dennis A. – TampaAlliance Insurance saved me over $500 a year on my auto insurance. Plus they were able to get me affordable home insurance and flood insurance to cover all my needs. Thanks to Pearce and all the crew at Alliance Insurance.”

David L. – St AugustineAlliance Insurance saved me hundreds on my Workers Comp, General Liability, Group Health and Commercial Auto and Insurance needs. Thanks Alliance. I will be recommending you to all my friends.

Tory H. – OrlandoMy Agent at Alliance Insurance shopped all the Auto and Home Insurance companies to see who gave me the best rate and plan. Alliance’s agents are knowledgeable and very polite. I will put all my insurance’s with Alliance. Thanks for the savings!”

John H. – JacksonvilleAlliance Insurance is the place to shop for all your insurance needs. I packaged my home and auto together and saved over $300 a year. My agent shopped around and got me the best rate. I would recommend everyone to use Alliance Insurance for finding the best insurance rates.

Mary S. – Tampa, FLI just saved over $400 on my Homeowners Insurance Florida with Alliance Insurance. My agent was very helpful, got me discounts I did not even know about and shopped all the carriers to make sure I was getting the best deal. Thanks Alliance! I will recommend you to everyone.

Joan P. – Orlando, FLYou all have access to the most companies and got us the best price on our coverage.

Jay Johnston, Jacksonville, Fl